Business credit cards are a valuable secret, usually offering larger welcome bonuses than personal cards and unique opportunities to earn huge travel rewards for business expenses like advertising, computers and phone bills.

It is easy to feel overwhelmed when you first encounter a business credit card application; they tend to be longer and more detailed than those of personal credit cards. But don’t worry — we are going to walk you through the process to fill out a Capital One business credit card application.

Who is eligible for a business credit card?

People are often afraid that they might not qualify for a business credit card account.

You don’t need to be a Fortune 500 company in order to qualify; business cards are for businesses large and small. Even freelancers or independent contractors can qualify. You can use your Social Security number as your business tax ID if you’re a sole proprietor.

You can qualify for a business credit card from side work that you are doing like ride-share driving, freelance photography and more. Many of our readers have qualified using businesses that only earn part-time or side income.

How to fill out a Capital One business credit card application

The process of applying for a business credit card from Capital One is similar to that for a personal credit card. There are just a few additional sections that ask questions which are specific to your business.

Throughout this demo I will be using the Capital One Spark Miles for Business application. But all applications for all Capital One business cards are essentially identical.

Let’s get started.

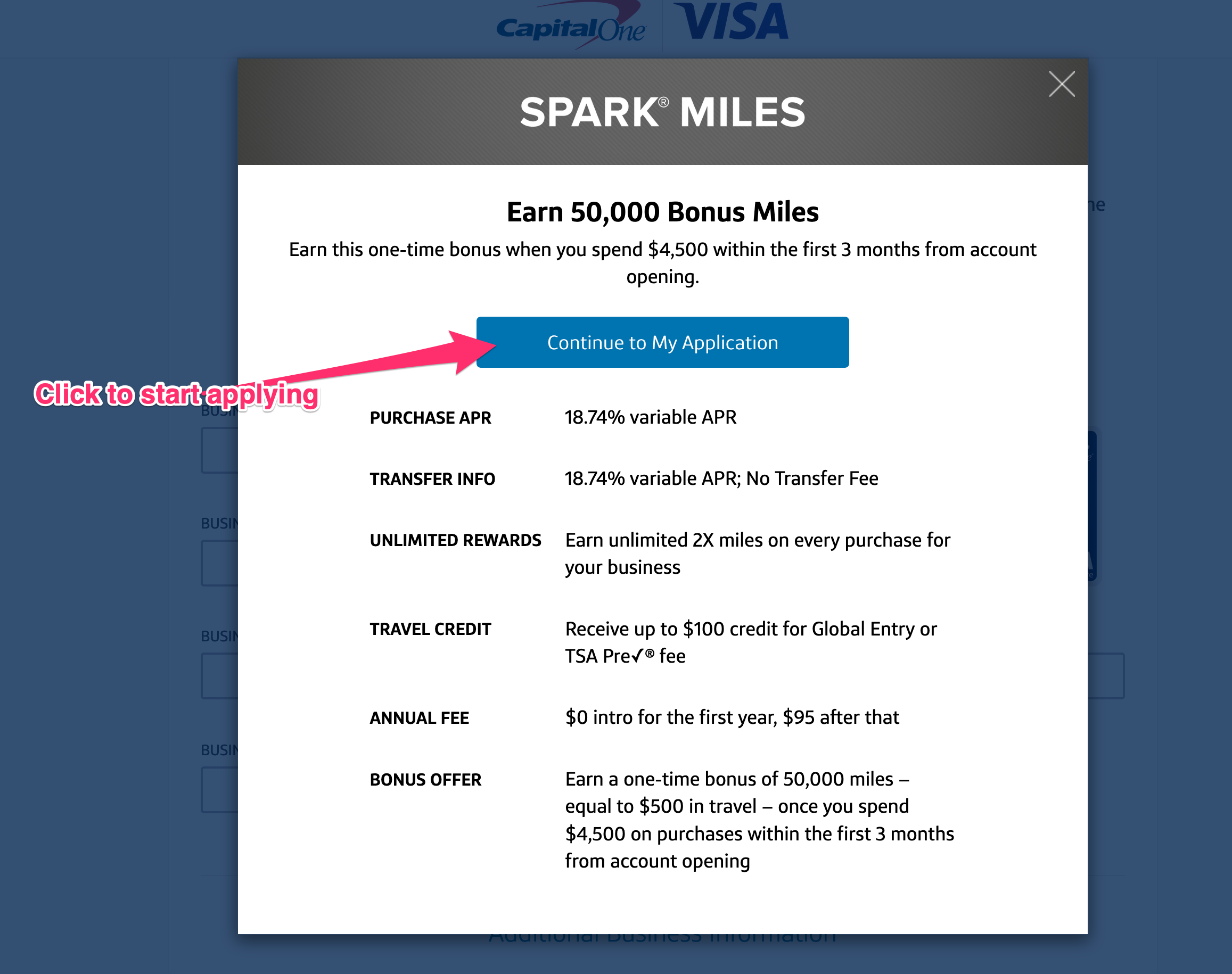

Step 1: Review offer details and start the application

After you click to apply for a new card with Capital One, a tab or window will open in your browser allowing you to quickly review the card and the offer details.

Review this information to make sure you are applying for the offer that you expected. Then you can click the big “Continue to My Application” button.

Step 2: General business information

Once you get to the application, the first information it requests is general information regarding your business. This is pretty simple to fill out, so go ahead and do it.

Business name: Be sure to enter your full legal business name here, if you are a sole proprietor it can be your name.

Business name as you want it to appear on the card: This is where you can enter the name that to be displayed on the card. Many people will simplify or shorten the name here. For example the legal business name might be “Acme Widgets Inc” and they will want the card to simply say “Acme Widgets.” It will default to your legal business name if you don’t override it in this field.

Business address: This should be the actual address where you have registered your business. This cannot be a post office box or CMRA location (like a mailbox at the UPS Store or Mailboxes Etc.). If you don’t have a physical office yet, then this can be your home address.

As you type in the address, it will autocomplete to valid known addresses. As soon as your address pops up, be sure to select it in order for the form to work.

Business phone number: This should be the main public phone number for your business. You will have an option later in the application to provide a primary contact number for your account (like your cellphone). For now you can add the main number for your business. If you are applying for a large business, it would be best to provide the main number for your corporate office (not a customer service line). For a freelancer, this might be your cellphone if you don’t have another business telephone.

Step 3: Business details

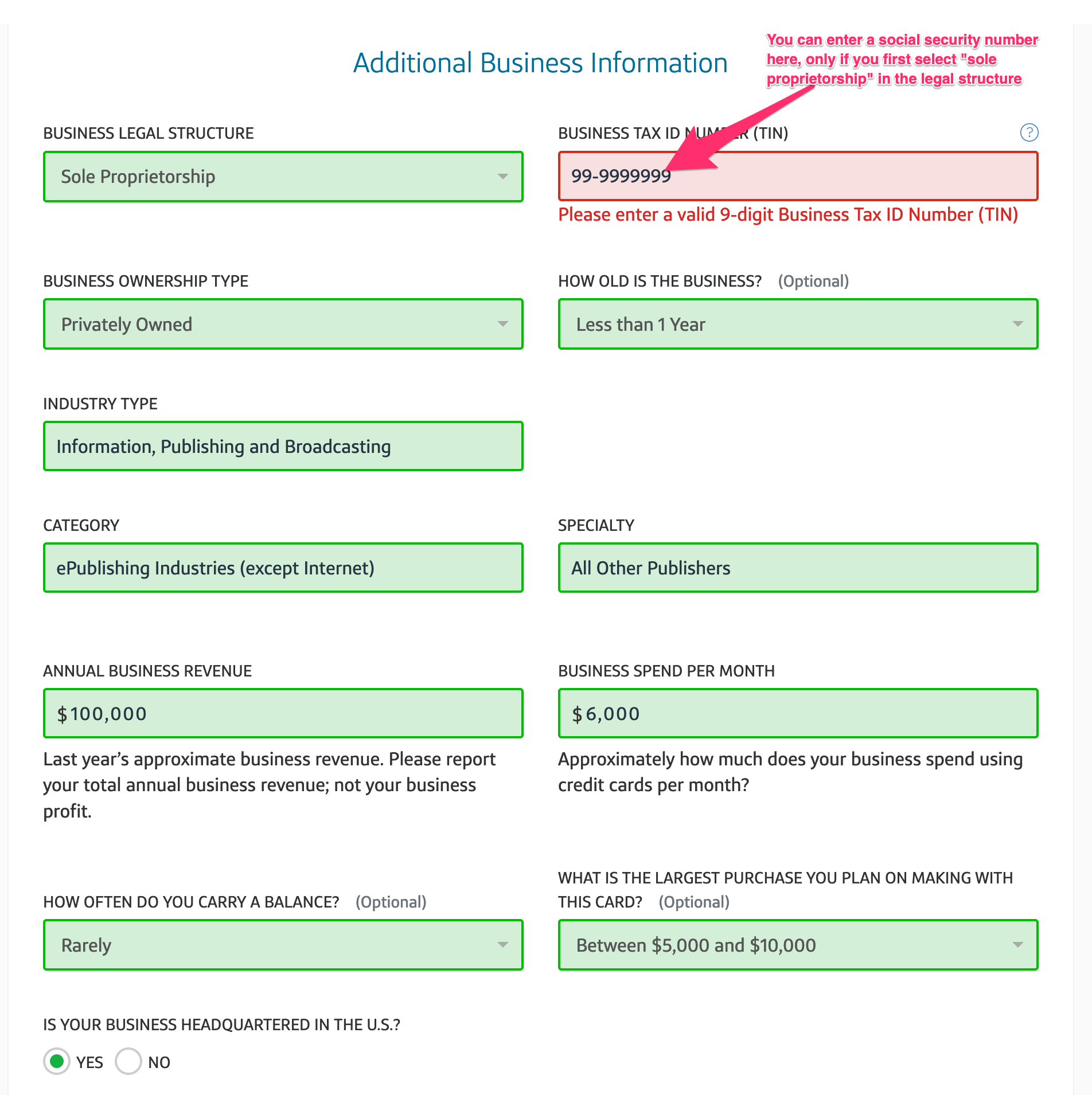

This is the section that gives most people anxiety when applying for a new business credit card. You are being asked to provide specific details about the business and how it is set up. We will break it down to keep it simple.

Some of these fields are optional, but it is a good idea to fill out as many as you can or make intelligent estimates for those fields.

Business legal structure: If you know how your business is structured (such as an LLC or corporation) then select the correct option here. If you don’t have a legal structure and you are the sole owner, then you will want to choose the “Sole Proprietorship” option. As a sole proprietor you can use your Social Security number as the business tax ID.

Business tax ID number: Established businesses with many employees should know their tax ID number and enter it here. If you were able to select “Sole Proprietorship” in the previous field, then you can enter your Social Security number here instead.

Business ownership type: Your options for this field will depend on what you selected in the “business legal structure” field. Most businesses will select “privately owned” here. And if you don’t know, this is the correct response. There may be options for publicly traded (meaning your business has a stock symbol) and for government-owned businesses too.

How old is the business: This optional field allows you to distinguish how long you have been running this business. Be honest with your response.

Industry type, category, and specialty: These are broken into three fields. Each field will have options that change based on the previous field. The idea is to identify what your business does. Each field will get more specific about the type of business you are operating. Use your best judgment to identify what you do.

Annual business revenue: This is where you can enter the revenue of your business for the previous year. If you have been in business for less than a year, enter a realistic estimate based on your year-to-date earnings so far. Keep in mind that this is asking for your revenue, not profit.

Business spend per month: Enter a realistic estimate of what you expect to put on your credit card each month. This is total card spending, not the balance you intend to carry.

There are a few other fields you should be able to answer with ease. This includes a few optional fields about the size of purchases you plan to use your card for and how much of a balance you intend to carry each month. Followed up by a few yes/no questions.

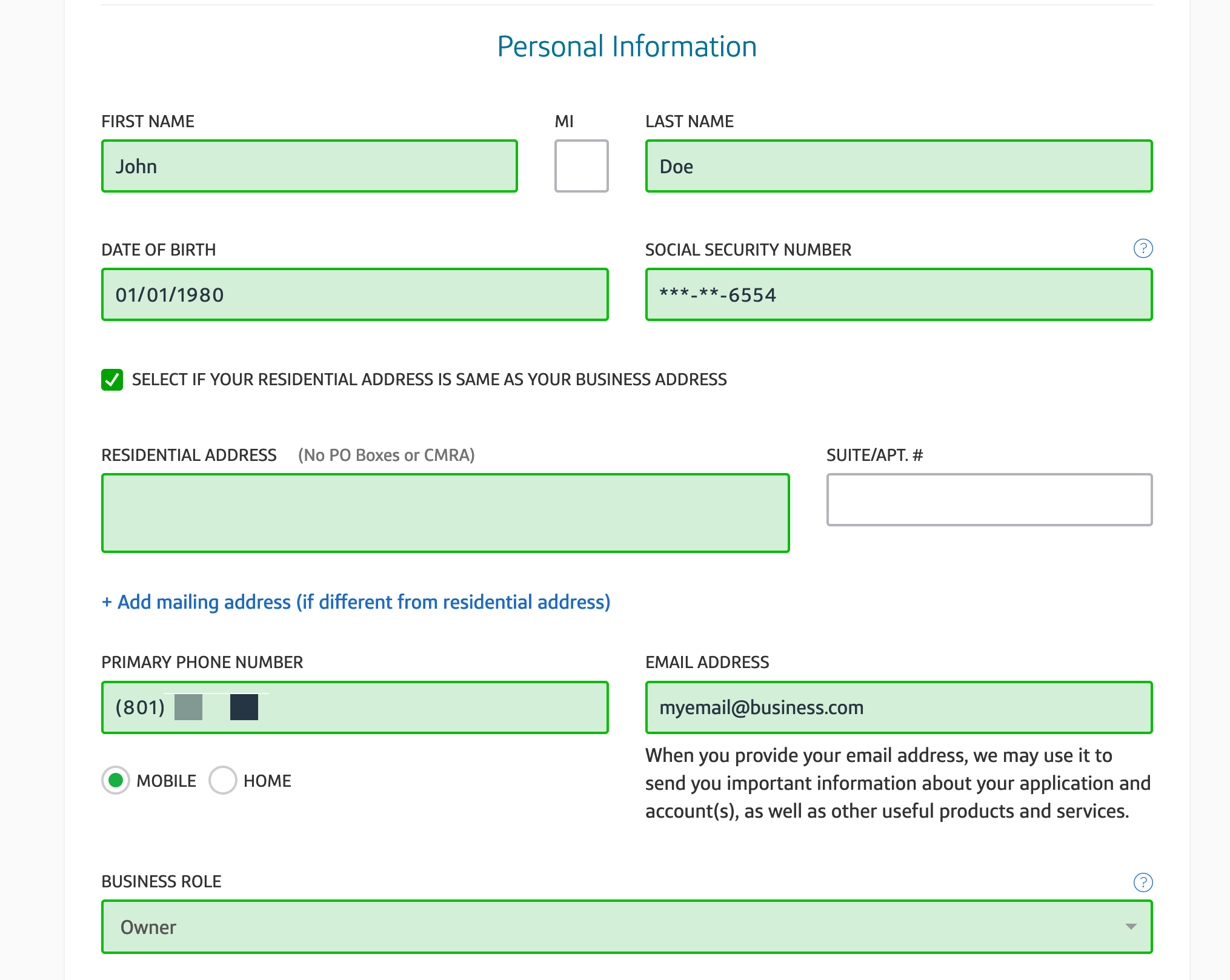

Step 4: Personal information

This section looks a lot like a normal credit card application. This is the place where you tell Capital One about you as the primary owner of this account. It will ask you to enter your legal name, Social Security number, address, and other financial details.

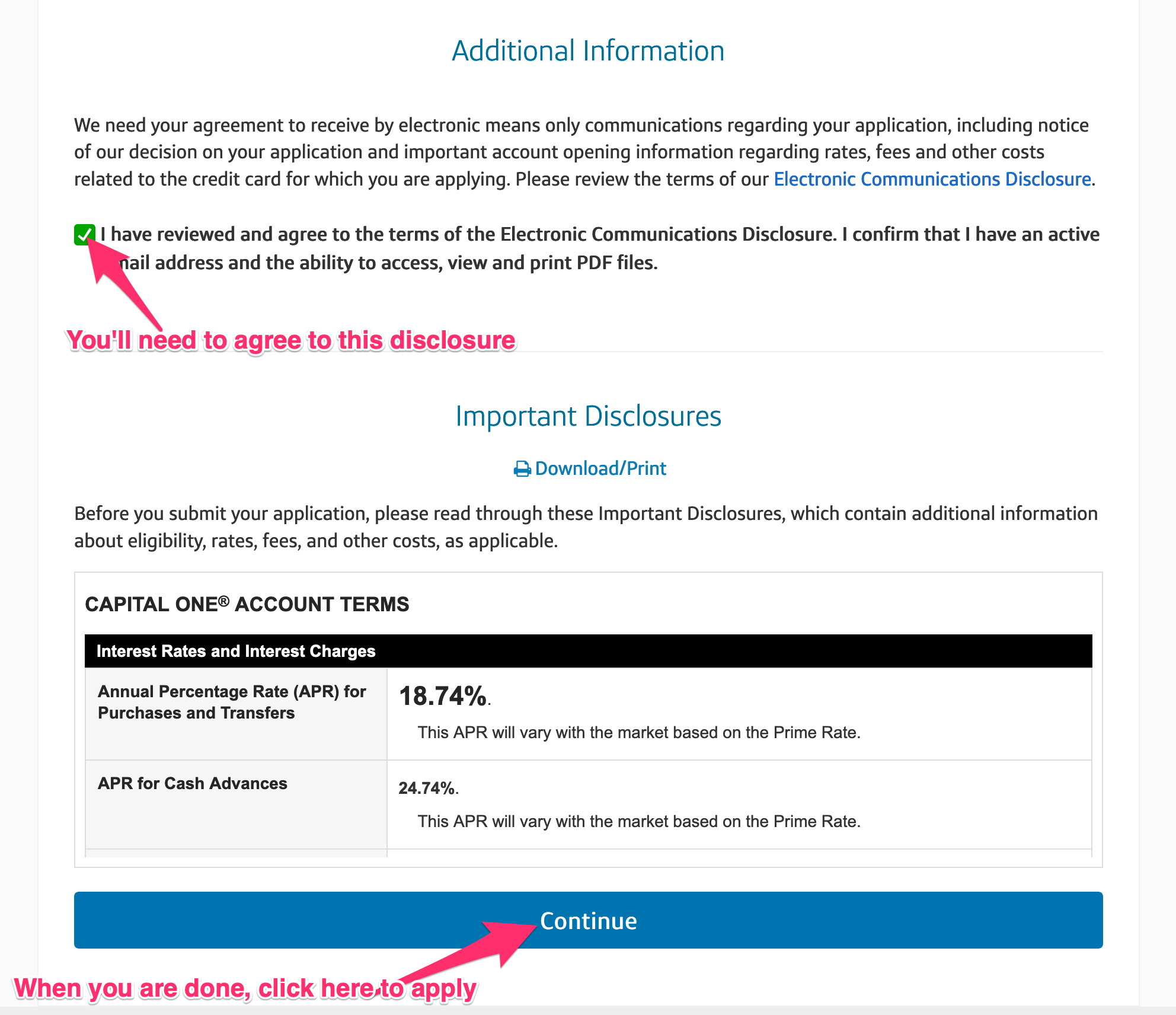

Step 5: Agree and apply

You are almost done. There are a just a few things to review and agree to.

If you are a corporation or LLC, you will need to provide information about anyone who owns more than 25% of the business. You will also need to agree that you have authority to apply for a card for this business. These options won’t appear for everyone, so don’t be worried if you don’t see this.

The next thing to agree to is the Electronic Communications Disclosure. Basically they just want to make sure that you can receive electronic updates (via email) about your account.

Finally, at the bottom you will see the terms of your account. This includes all the standard credit card information like an overview of benefits, interest rates, and other important details. There is an option to download this as a PDF to your computer or to print. You can also scroll through and read it directly on the page.

When you have read the terms, you can click “Continue.”

Capital One will show a condensed version of the application for you to double-check and review. Be sure to read this over to make sure that everything looks accurate. When you are done, you can click the large green “Submit Application” to process your application.

Wait for a response

You should get a response back in less than a minute about whether you were approved or denied for a card. However, in some cases you might be asked to wait 7-10 days for a response.

If you get this response, it is usually best to wait for an official approval or rejection from Capital One before doing anything else. Often they just need to verify one piece of information before they approve you, so don’t be immediately worried if you see this.

If you are rejected, then you can always call for reconsideration. Unfortunately, Capital One doesn’t offer a dedicated reconsideration line, but you can call their small-business credit card support number at 1 (800) 227-4825.

Our favorite Capital One credit cards

- Capital One Spark Miles for Business — Earn 50,000 miles after spending $4,500 on purchases within the first three months of account opening. Earn 2x miles 0n every purchase; $95 fee, waived the first year.

- Capital One Spark Miles Select for Business — Earn 20,000 miles after spending $3,000 on purchases within three months of account opening. Earn 1.5 miles per $1 on every purchase; no annual fee.

- Capital One Spark Cash Select for Business — Earn $200 cash bonus after you spend $3,000 on purchases within three months from account opening. Earn unlimited 1.5% cash back on business purchases; no annual fee.

The information for the Capital One Spark Miles, Capital One Spark Miles Select, Capital One Spark Cash, Capital One Spark Cash Select card has been collected independently by Million Mile Secrets. The card details on this page have not been reviewed or provided by the card issuer.

Bottom line

Applying for a Capital One business card is easy; it doesn’t have to be daunting or overwhelming. Take it step by step and you can be finished in no time.

Once you start using a business credit card to pay your business expenses, you will be surprised at how quickly the rewards start rolling in. Businesses have expenses that must be paid, so using a credit card is an excellent way to earn rewards toward free travel when paying them.

If you want to learn more about credit card rewards and see more guides, subscribe to our newsletter.